Updated April 11, 2023

Raymond Micaletti, Ph.D.

Alpha

The market was relatively quiet during last week’s holiday-shortened affair. The broad U.S. equity market was down half a percent, while the S&P 500 finished flat and the Nasdaq 100 was down just shy of 1%. All are still sporting solid gains on the year.

While the market was quiet, the economic data released last week spoke loudly and clearly–the economy is unquestionably softening, especially on the jobs front.

We had four pieces of jobs data released last week: the JOLTS job opening data, the ADP non-farm employment change, the weekly initial jobless claims data, and the Bureau of Labor Statistics' non-farm employment change.

The JOLTS and ADP numbers were much weaker than expected, coming in at 9.93 million job openings (vs. 10.5 million expected) and 145k new jobs (vs. 208k expected), respectively.

Initial jobless claims were also weaker than expected, coming in at 228k vs. 200k expected. More telling, however, was that the numbers from previous weeks were revised higher. For example, the previous week’s 198k number was revised to 246k initial claims.

The week was capped off by the Friday release of the non-farm payrolls (NFP) number, which came in slightly ahead of estimates (236k vs. 228k expected). However, the number of new jobs added in the private sector–189k–was the least since late 2020.

Clearly, the job market is slowing. But jobs data wasn’t the only data that disappointed last week. Both manufacturing and services PMIs also came in weaker than expected.

Higher interest rates are finally taking their toll on the economy.

The stock market was closed on Friday, and today’s reaction has been generally neutral.

This week will likely bring more clarity to those rate expectations as we get data on inflation (both the CPI and PPI), retail sales, and a slew of bank earnings (which will hopefully provide some perspective on the ongoing bank crisis).

Amidst all that, what can we expect from the never-ending battle between the bulls and the bears?

On the bullish front, there have been some interesting developments:

On March 31, another equity market breadth thrust triggered–this time a Zweig Breadth Thrust (ZBT) (named after its creator, Marty Zweig). This follows on the heels of the Breakaway Momentum (BAM) breadth thrust that triggered on January 12. While BAM has been successful in 24 out of 25 occurrences (i.e., the market was higher 12 months later in 24 of 25 cases), ZBT has never had a failed signal across many decades (although that doesn’t in any way guarantee the current signal will be successful).

Along similar lines, when the market has been down for a calendar year and then has rebounded in the first quarter of the next year–as has happened in 2022 and 2023–the market has never finished the year lower than its first quarter closing price. Thus, if history were to hold, we would expect the market to continue to rise over the balance of the year.

Speculators continued to short the market to an extreme degree this past week. The current level of speculator bearishness has been eclipsed only three times in the past five years. As Goldman Sachs trader, Bobby Molavi, wrote this week, “Most are positioned and believe the market will break to the downside…yet it seemingly never does.”

But the bearish items keep accumulating as well:

Speculators (who tend to get the direction of the dollar correct) are buying the dollar again. While their relative positioning is still bearish compared to retail traders, their level of bearishness is rapidly decreasing. Indeed, if speculators’ recent pace of buying continues, we may see dollar relative sentiment turn bullish in the next few weeks. Bullish dollar relative sentiment would likely lead to increased real rates and tighter financial conditions–both of which would be negative for equities. This is definitely something to keep an eye on.

While speculators have greatly increased their short positions, institutions have not increased their long positions at all in the last couple weeks. Who has then? Retail investors. As a result, the relative sentiment between institutions and retail investors, while still bullish, has become less so. If institutions don’t step up their buying in the next few weeks, we could see equity relative sentiment (which has been bullish since June 2022 when the S&P 500 was at ~3650) turn bearish in early-to-mid May.

As discussed earlier, economic data has been mostly weaker than expected in recent weeks. The Atlanta Fed GDPNow estimate has fallen from 3.2% in mid-March to 1.5% this past week–that’s a fairly steep decline in just three weeks.

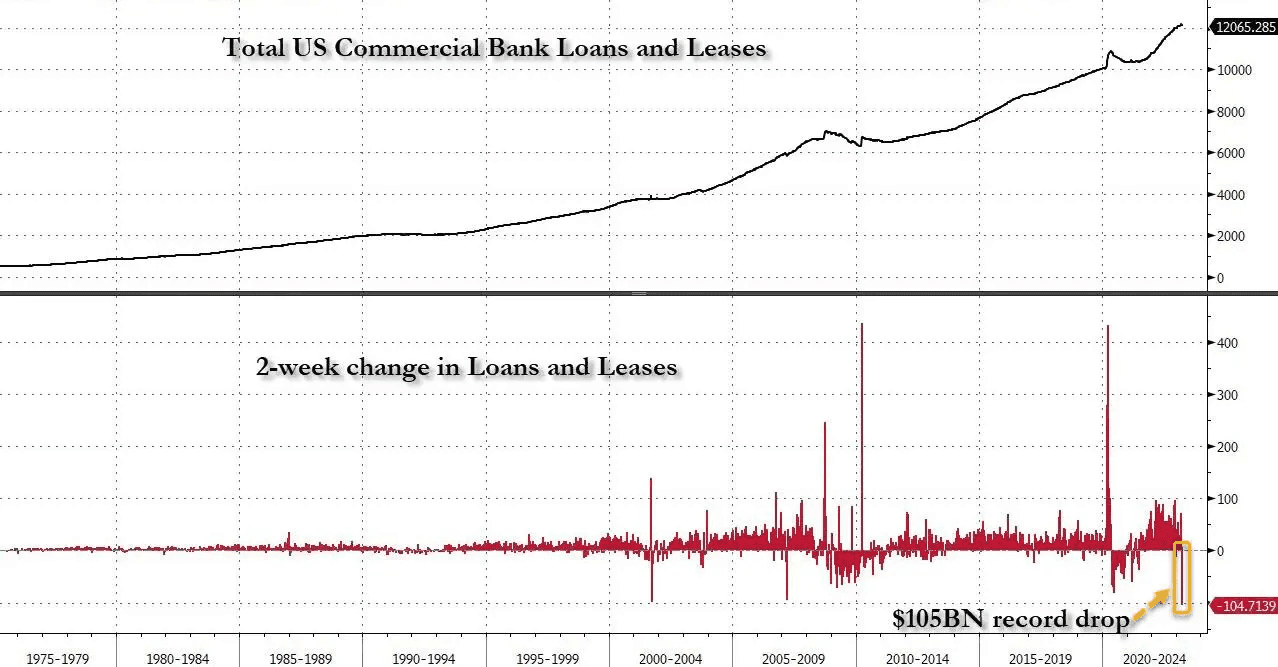

The last two weeks of March saw the biggest two-week drop in lending by commercial banks on record. This drop in lending was due to the ongoing outflow of deposits (as banks had to monetize existing loans to redeem depositors who took their money elsewhere; thus, banks were not making new loans as their asset levels fell).

Source: ZeroHedge

Commercial real estate (CRE) appears to be the next shoe to drop for banks, as several hundred billion dollars worth of CRE loans need to be rolled over at higher interest rates later this year. But with nearly 1-in-5 commercial properties vacant and not receiving any rent payments, many of those loans will likely default, further exacerbating the bank crisis.

Despite the slowing economy, the market is now forecasting an additional rate hike at the Fed’s May meeting. Needless to say, higher short-term interest rates would not help the slowing economy.

Energy-related commodities have jumped recently, spurred in large part by the OPEC+ production cut announced last weekend. As a result, retail sentiment in those assets has also jumped and is now approaching levels that suggest inflationary pressures are rising. When commodities sentiment reaches those inflationary levels (we’re not quite there yet), it tends to be a headwind for equities.

Thus, the conflict between bullish positioning and bearish macro reality continues…

The Bull Case

The bull case for equities is that positioning wins out: financial conditions continue to ease (as the Fed and perhaps other central banks inject liquidity into the system to help stem the bank crisis), and shorts are forced to cover their positions.

The Bear Case

The bear case for equities is that economic gravity wins out: the dollar stops going down, financial conditions tighten, real rates rise, and the Nasdaq, which has dragged the entire market higher this year, falls to a more justified level.

Our View

This week’s call is more difficult than in previous weeks, where we had repeatedly leaned toward the bull case. But now that speculators are buying the dollar, retail investors are getting more bullish on equities, and commodities sentiment is close to becoming a headwind, market direction is not as clear cut, especially with the noticeably softer economic data.

That all said, until dollar relative sentiment turns bullish or equity relative sentiment turns bearish (and neither is quite there yet), we believe the extreme short positions of hedge funds coupled with the recent breadth thrust will serve to keep equities supported in the near term.

But unless institutions step up their bullishness relative to retail traders in the coming weeks, the shelf-life of this bull run may expire in early-to-mid May, which would line up well with the market adage, “Sell in May and go away.”

Let’s see how it plays out.

At Allio our strategic portfolios remain positioned for the secular macro regime we find ourselves in—one driven by high and sticky inflation. As a result, our portfolios are tilted toward commodities, energy stocks, gold, emerging markets, and inflation-protected bonds. We also have ample allocations to T-bills with their currently high yields.

On the tactical front, we will be looking to enter QQQ on any pullback and will be keeping an eye on bank earnings this week to see whether the large recent dip in the sector represents an opportunity or a falling knife to be avoided.

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.