Updated April 18, 2023

Raymond Micaletti, Ph.D.

Alpha

Another week, another gain for the broad U.S. equity market, which has been up four out of the last five weeks (for a gain of 6.5%) since the collapse of Silicon Valley Bank.

Last week was a big one for economic data and the results were mixed, but generally favorable.

Inflation, both the CPI and PPI, came in at or better than expected, while consumer sentiment was also pleasantly above expectations.

The one major miss was retail sales, which may have reflected a consumer slowdown on account of the banking crisis.

There’s no crisis with the big banks, however. Earnings from JPMorgan, Citi, Wells Fargo, and Bank of America all were solid and the S&P 500 financial sector was up over 2% last week.

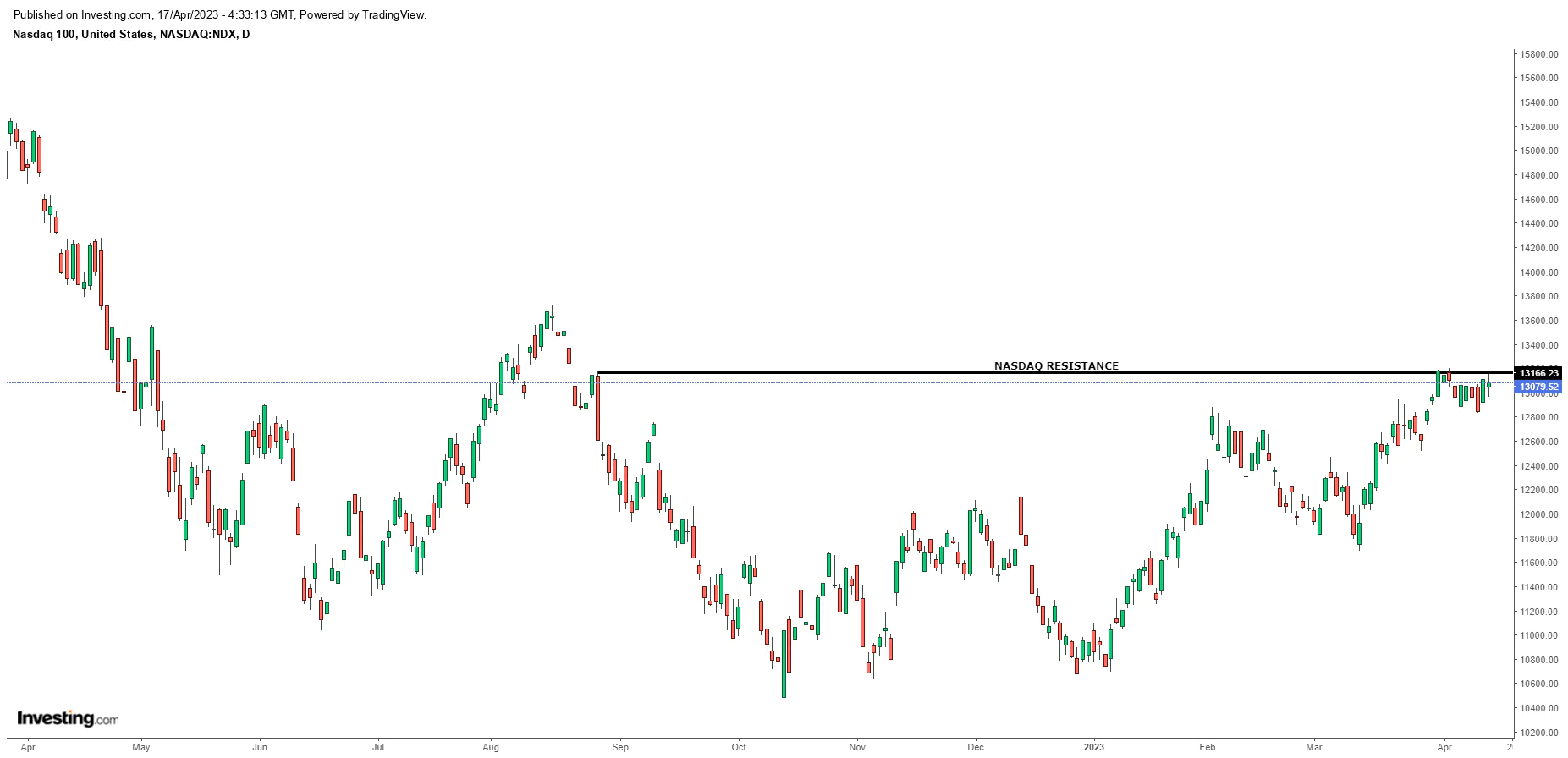

Now the major equity indices, particularly the S&P 500 and Nasdaq 100 sit just below resistance levels (4200 on the S&P futures, 13,200 on the Nasdaq futures).

Source: Investing.com

Will they finally be able to break through, or will we witness yet another failed attempt?

Earnings season, which will start in earnest this week, should bring clarity one way or the other.

On the plus side:

Seasonality is favorable. According to technical analyst Wayne Whaley, the week of April 15-22 has been up 68% of the time since the last 50 years for an average gain of 0.72%.

A Zweig breadth thrust triggered recently. Only 14 have triggered since 1950. In all cases, the market was higher both 6 months and 11 months later. Notably, such signals have tended to trigger near the beginning of bull markets.

Institutions resumed their buying of equities last week–at a strong clip–after a brief respite the prior week. Retail investors were selling. Such a combination tends to bode well for equities in the near- to intermediate-term. Notably, institutions have had many opportunities to sell equities the past six months and have shown no inclination to lessen their equity exposure.

Other positioning and sentiment metrics remain supportive for equities. Though not quite as favorable as in recent weeks, they are still far from levels that would represent headwinds for equities.

On the negative side:

The higher the market goes, the worse the already-bad valuations get. The disconnect between interest rates and equity indices continues to linger. The 10-year Treasury yield (3.5%) is 0.3% percent higher than the expected long-term annualized U.S. equity return (3.2%), which suggests there will be a reckoning at some point in the future to bring valuations to more reasonable levels, especially given the likelihood of persistently high inflation.

The move higher in equities this year has been driven mostly by megacap technology stocks. If those pull back meaningfully, they would likely bring the entire market lower.

The Treasury General Account, which in recent weeks has poured several hundred billion dollars into the financial system–equivalent to a round of quantitative easing–as the Treasury deals with the debt ceiling limitations, is running low on cash and thus future injections of liquidity may dry up

If liquidity does dry up, the dollar will likely rise, which would also tend to drive real rates higher. Higher real rates would likely slam the brakes on the equity rally. Notably, while dollar relative sentiment remains bearish, it is at its highest level since last December and within shouting distance of turning bullish.

The market is pricing in an 80% chance of another rate hike in May and several Fed speakers resumed their hawkish jawboning this past week. Thus it may take another flare up of the bank crisis to get the Fed to soften its rhetoric.

Speaking of banks, the S&P regional banking index is still near its recent lows despite strong earnings from the big banks–i.e., the market appears to be saying that small and mid-sized banks are not out of the woods yet and there may be more bank failures to come.

Source: Investing.com

The wild card in all of this is earnings.

Earnings expectations have been significantly lowered in recent weeks. As a result, it may be easier for companies to beat those lowered estimates. Moreover, analysts expect Q1 to be the low point for corporate earnings. Consequently, even if earnings disappoint, if company outlooks are optimistic, equities may still respond favorably.

In the tech sector, the weaker dollar and lowered labor costs from extensive layoffs may bolster earnings. The question is whether the strong tech rally has anticipated these potentially higher earnings and thus will announcements of such be “sell the news” events?

The Bull Case

The bull case for equities remains one of positioning. Institutions continue to buy relative to retail traders and speculators. While institutions don’t always win, it also doesn’t pay, long term, to fade them.

The Bear Case

The bear case for equities continues to strengthen. Equities are at resistance and until they break through, it’s plausible they will first have to go lower before making another attempt higher.

Liquidity injections from the Fed (as a response to the banking crisis) or Treasury (to deal with the debt ceiling), which have increased in recent weeks, look set to decrease or disappear altogether.

Positioning may be near to flipping on the dollar, which would likely cause the market to switch to “risk-off” mode.

And again, valuations are unattractive and the disconnect between rates and valuations persists.

Our View

Despite the burgeoning bear case, we believe the odds still favor more upside for equities before the market changes direction for a sustained period. Those odds, however, are not as high, in our opinion, as they were several weeks ago. I.e., we may be getting closer to a turning point.

The market keeps knocking on the door of resistance. The more times it knocks, the more likely the door will eventually open.

If the door does open, what we would then look for is a major squeeze higher in equity indices–perhaps brought about by better than expected earnings in a seasonally strong period–such that the market narrative shifts from one of doom (“recession,” “hard landing,” etc.) to one of hope and optimism.

Such a shift would likely force speculators and retail traders to finally give up on their short positions and allow institutions to happily sell the equities they had bought in the 3500-3600 area on the S&P 500.

We would note that institutions went nearly a year being bearish on equities from July ‘21 to June ‘22, during which time equities lost 18%. It’s now creeping up on a year that they have been bullish and equities have subsequently risen 16%.

Thus, until institutions turn bearish, it’s hard for us to be bearish. Their collective wisdom is likely to trump our personal market opinion the vast majority of the time.

Allio Portfolio Updates

We took a tactical position in the Nasdaq 100 this week after a small pullback, as its technicals and positioning suggest it could see further upside.

Otherwise, we remain positioned to weather the overarching secular regime of higher inflation and (eventually) negative real interest rates with our tilts toward gold, commodities, and energy stocks.

Download Allio in the app store today to get your own automated investment portfolios managed by real experts.

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.