Updated June 20, 2023

Raymond Micaletti, Ph.D.

Macro Money Monitor

Market Recap

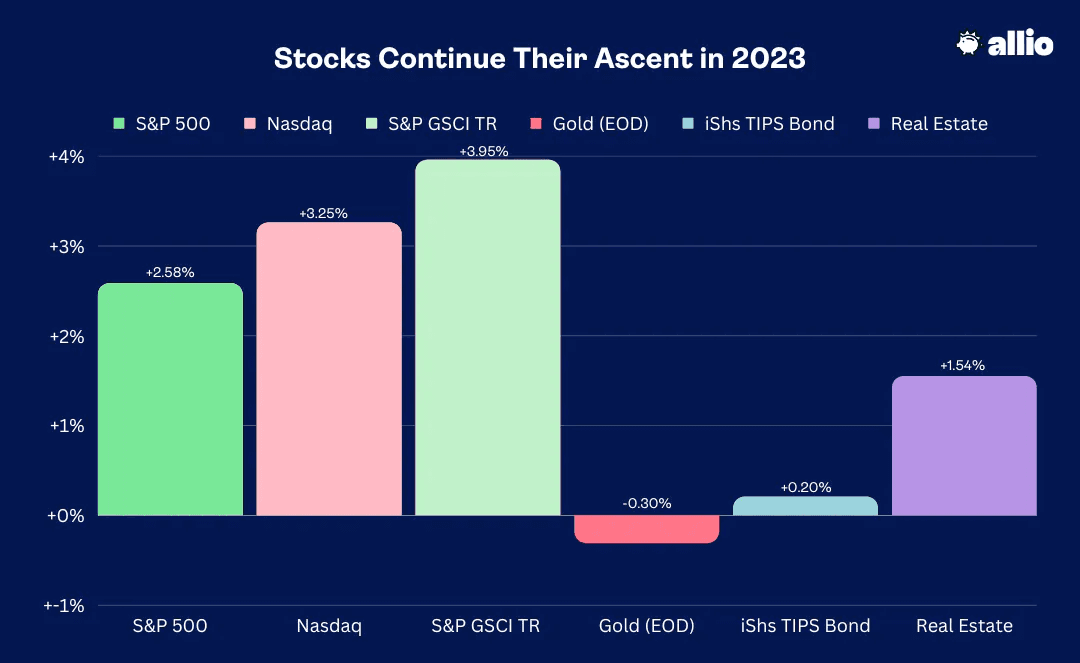

Stocks took May CPI data and the June Fed ‘skip’ in stride. The S&P 500 rose 2.6% (now +23% from the October 2022 low) while the tech-heavy NASDAQ Composite outperformed with a 3.3% advance to notch fresh 52-week highs. Both the growth Technology sector and cyclical Industrials space have posted impressive gains lately, and we’ll get a macro read from FedEx (FDX) in its Q2 earnings report Tuesday night this week.

The Real Estate sector, meanwhile, underperformed as interest rates meandered, but still sported a 1.5% climb. There were finally some signs of life across the commodity complex, though gold finished fractionally lower. Inflation-protected bonds ticked up amid an ever-steepening Treasury yield curve, while overall fixed-income volatility managed to end last week at its lowest level since February.

June 9, 2023 - June 16, 2023

The Fed Takes a Breather

As expected, the Federal Reserve paused its rate-hiking cycle last week after 10 straight policy rate increases. It was viewed as a ‘hawkish hold’ as Chair Powell aimed to anchor traders to the FOMC’s plan to raise its policy rate two more times before the year’s out. While few on Wall Street believe the target rate will be near 6% by Christmas, rate traders have at long last succumbed to the Fed’s firm stance that no rate cuts will happen this year.

As it stands, the current target range of 5% to 5.25% is seen as inching higher by just one additional quarter-point move come the July 26 Fed gathering. Then comes the much-anticipated pause. The market expects a very gradual easing of monetary policy next year, but there’s nuance to this probability that not many analysts describe.

The reason why it appears as if the bond market has gotten it wrong—initially pricing in cuts during the second half of this year, but not aligning itself with the Fed’s outlook—is that there was always the chance of an economic slowdown as 2023 progressed. And that could still happen, but it is looking increasingly likely that no technical recession will occur. So, the Fed Funds futures market is constantly weighing the chance of some kind of turn of events that would lead Powell to have to cut rates unexpectedly. That hasn’t happened. As long as the economy holds up, the more we will continue to have the ‘higher for longer’ mantra play out.

Along with this probabilistic thinking about how interest rates unfold, it’s key for investors to realize that the Fed Funds futures market is mainly a hedging mechanism for major Wall Street banks. Thus, it often underplays what the true benchmark policy rate will be.

Regardless of the mechanics, we are in a new world of 5% short-term yields while stocks now trade near 20 times forward earnings estimates.

Are Equities Due for a Summer Swoon?

So, investors must now ask themselves, “Are stocks too pricey today?” The S&P 500 has returned more than 15% in 2023 while the Nasdaq 100 ETF is up nearly 40%, on pace for one of its best first-half performances on record. Small caps have only recently begun to participate, and that island of misfit equities is higher by just 7% YTD. The valuation picture is not as sanguine as it was during the fourth quarter of last year.

The SPX now sells for a significantly more expensive amount relative to its 30-year average forward price-to-earnings ratio of 17.3. What’s different this time is that we now have a risk-free Treasury rate in excess of 5%, so that would hypothetically warrant a lower valuation multiple on stocks. The bulls can counter with the reality that we may be on the cusp of a productivity boom care of artificial intelligence, justifying a higher fair P/E.

We have been insistent on a melt-up kind of market over the last few months, led by the tech trade. But as stocks continue to rise, now almost in a parabolic fashion, the likelihood of a correction increases. Thus, the risk/reward condition in equities is significantly more precarious now than when positioning and sentiment were so bearish just six months ago. As a result, we exited our tactical long position in the Nasdaq 100 and will be on the hunt for new opportunities this summer.

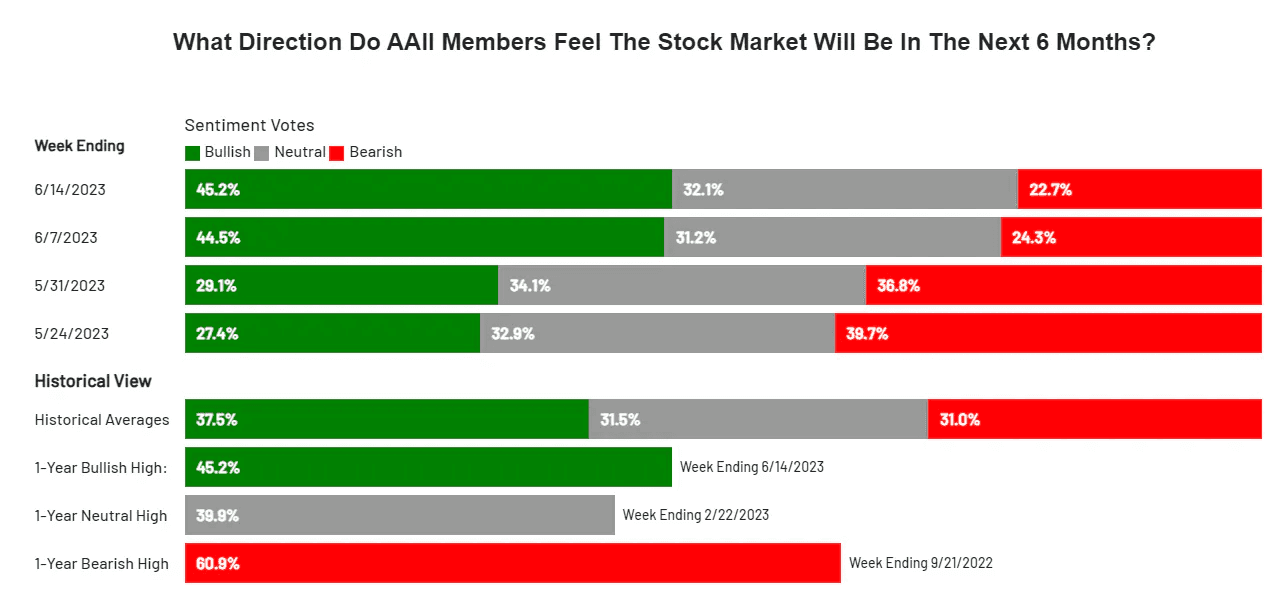

The Bulls Might Be Here to Stay

What could keep stocks on the ascent is only the very recent turn from fear and doubt to greed and hope. Like last week, eyeing the AAII sentiment survey provides key clues into the retail investor psyche. The most recent findings show yet another uptick in net bulls. At 45.2%, it is the highest bullish reading in the last year. What does this mean for the stock market? FOMO could very well continue, but as more folks climb on board the optimism bandwagon, its wheels become all the more strained.

Happy Days Are Here Again: Back-to-Back Bullish Sentiment Surveys

Source: AAII

May CPI: A Snoozer!

But let’s widen the scope. It was a busy week indeed. Last Tuesday’s May CPI report came and went without much fanfare. Contrast that with how much inflation data rocked markets in 2022. The monthly 0.1% rise in the headline rate matched economists’ expectations while the core rate (ex-food and energy) was higher by 0.4%. It was the softest annual measure since March 2021 and marked 11 consecutive months of sequential inflation drops.

Recall it was a year ago when oil prices peaked, so after the June report due out during the middle of next month, the ‘comps’ become less rosy for inflation doves. Not surprisingly, last Friday, two officials, Fed Governor Christopher Waller and Richmond Fed President Thomas Barkin reiterated the need for more tightening. It appears good ole FOMC jawboning is back in play in this final Fed thrust to clamp down inflation for good.

Producer Price Trends Tumble

Perhaps more encouraging was the often less heralded PPI report that was released hours before the Fed decision last Wednesday. The headline rate matched the consensus estimate, but a flat month-on-month core rate was much better than expected. That could be a boon to corporate profit margins (should the trend persist) as 2023 wears on.

Jobless Claims in the Spotlight

What we were paying particular attention to last week were Initial Jobless Claims. It’s often no big deal since it comes out weekly and the survey of all 50 states has its quirks. Right now, however, all macro investors must give the report its due. On June 8, a notable rise in those filing for first-time unemployment benefits jumped. So, the June 15 report was critical since another week of increased claims would buttress the argument that the labor market is finally cooling with some gusto.

Indeed, a second consecutive 262,000 claims figure gives merit to that economic-cooling thesis. Once again two states (Minnesota and Ohio) mucked up the total tally. Still, a couple more soft weekly claims reports may result in a negative June monthly payrolls report. And that could lead to the dovish members of the Fed to back off from the current consensus of two additional rate increases this year.

Does the National Debt Matter?

That leads us to another significant macro risk few strategists are willing to bring up during this high time for the markets: labor market contraction ahead of a pivotal general election (that's now less than 17 months away).

The Democratic-controlled Senate and Executive branch will do everything in their power to keep the economy afloat as November 2024 nears. The last thing President Biden and incumbents on the left want is to see month after month of employment losses across the country. We’ll be keeping our eyes and minds open to the chance of additional stimulus packages and spending projects being announced over the ensuing quarters.

On that note, conservatives on Capitol Hill can attack spendthrifts on the opposite side of the aisle with one key figure. The US national debt has climbed to $32 trillion for the first time. While what the nation owes has never been a true cause for investor alarm, higher borrowing rates today versus those seen in the 2008 to 2021 period could make the debt problem come home to roost at some point. At the very least, expect Republicans to use it as a weapon against the current administration.

Consumer Spending Holds Up

Let’s ease the tension from political strife to something a bit lighter. Summer travel season is in full swing. Schools are out, PTO days are being put to work, and folks are hitting the road and taking to the skies. With gas prices down from near $5 this time a year ago to slightly more than $3.50 today, road trips are modestly more affordable.

Overall, travel spending trends are mixed. The May Advance Retail Sales report was largely in-line with forecasts last week. The Core Control group, what really matters in the survey, rose just 0.2% month on month. Card data from Bank of America has recently suggested that international travel spending has been robust, so we’ll see if the consumer keeps it up.

Families More Upbeat About Incoming Inflation

Sticking with the consumer topic, Friday’s University of Michigan Sentiment report was more than notable. We don’t care so much about consumer confidence most of the time, but how folks feel about inflation is key. The Fed pays close attention to it, and the more families expect inflation to rise, the more embedded rising prices tend to be.

The 3.3% 1-year inflation expectation print was one of the largest sequential falls in the report's history, though the long-run rate matched the consensus forecast. This is another signal the doves can point to that underscores the case the Fed has no business continuing to hike rates.

Buoying Consumer Sentiment

Source: Bloomberg

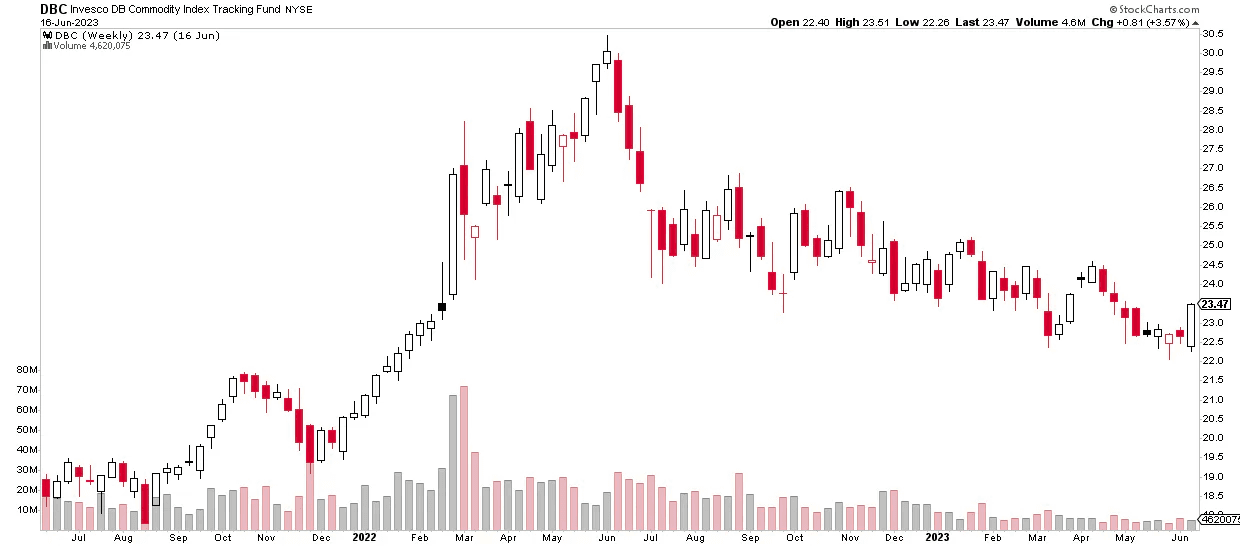

Commodities Rallying – the Start of a Trend?

Lastly, it’s time to give the commodities market some love. While gold shined for a moment this quarter as it approached all-time highs, the rest of the space has been sour. Oil is near $70 while copper has been embattled for much of the year. Last week, however, as most of the financial media were focused on the Fed and a rising stock market, it was the commodities complex that posted a notable climb.

Technicians call last week’s candlestick a bullish engulfing and a bullish marubozu. Funny monikers, yes, but it is seriously impressive price action that warrants attention. We acknowledge that the trend is firmly lower off the June 2022 peak, but a rise in commodities would catch not only investors off guard but also the Fed, which has been welcoming lower prices to quell inflation.

DBC Commodities ETF: Bullish Weekly Performance Flies Under the Radar

Source: Stockcharts.com

The Bottom Line

Stocks reached new highs as the Fed paused rate hikes and indicated two more increases in 2023. But concerns about pricey stock valuations and a possible market correction have emerged all while the FOMO train accelerates.

We are closely watching key economic data, including inflation and jobless claims, while the commodities market experienced a sly climb last week, potentially contradicting the Fed's efforts to control inflation through tight monetary policy. This week, we get key reads on the housing market, the state of industrial activity via FedEx earnings, and a first look at June Manufacturing and Services PMI figures on Friday.

Want access to your own expert-managed investment portfolio? Download Allio in the app store today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.