Updated July 11, 2023

Raymond Micaletti, Ph.D.

Macro Money Monitor

Market Recap

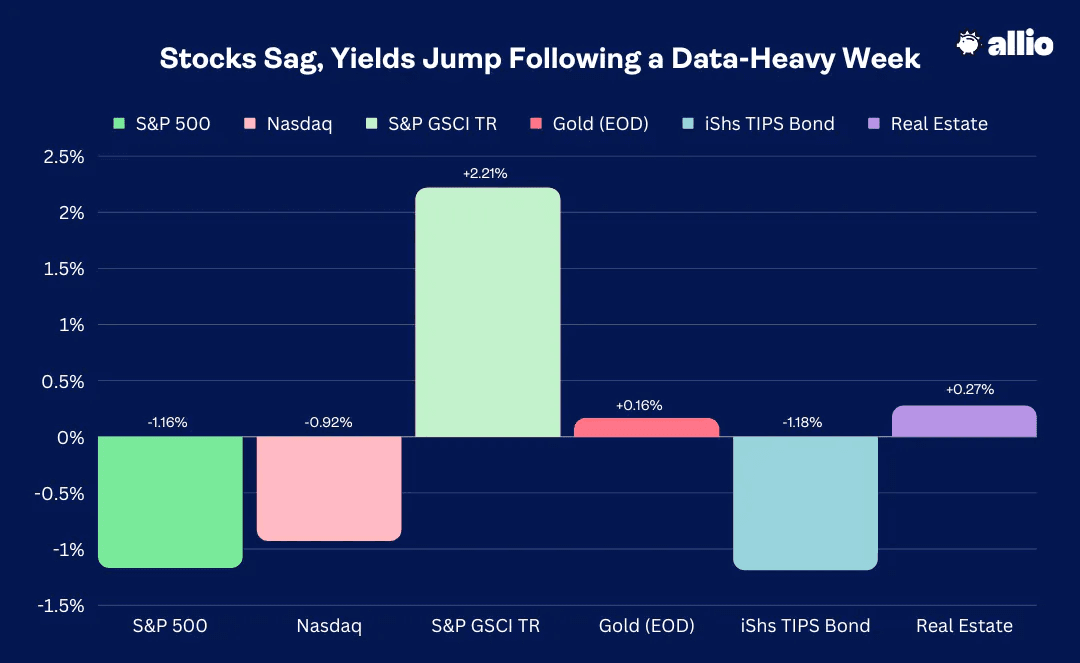

Stocks fell modestly last week as rising interest rates cast fears that the Federal Reserve will be more aggressive in its second-half interest rate path. The S&P 500 lost just 1.2% while the NASDAQ Composite gave back less than 1%. The best sector for the week (and it has been a while since we can report this) was Real Estate despite the jump in yields. Commodities, likewise, finished in the black as the US Dollar Index retreated. Gold, however, managed to post just a fractional gain during the first week of the second half and overall gold positioning remains neutral. As domestic bonds go, often so goes the TIPS market; inflation-protected fixed-income dropped about as much as the SPX.

Looking Ahead

While last week was headlined by key monthly manufacturing and services data, along with a plethora of labor market indicators, this week kicks off the second quarter earnings season with US CPI and PPI tossed in the mix. We’ll also get key monetary policy updates from the Bank of China, the Central Bank of Korea, and the Reserve Bank of New Zealand.

The Fed’s Beige Book, a summary of commentary on current economic conditions across the 12 Fed districts hits on Wednesday while minutes from the latest ECB meeting cross the wires Thursday morning. Finally, on Friday a first look at July University of Michigan Consumer Sentiment will be released at 10 a.m. ET.

Key earnings reports include Delta Airlines and PepsiCo on Thursday before the bell. The largest Dow component, UnitedHealth Group, reports Friday morning along with a slew of big banks.

Stocks Sag, Real Estate Outperforms, Yields Jump Following a Data-Heavy Week

6/30/23 - 7/7/23

Will the Real Jobs Market Please Stand Up?

We know a lot more about the state of the domestic labor situation today compared to a week ago, and yet it remains murky. The major employment data point that rocked both the stock and bond markets last week was the ADP Employment reading on Thursday morning. This report is released in advance of the official nonfarm payrolls report, and it is seen as a loose barometer of the state of the private sector jobs market. Now, typically the ADP figure is met with a high dose of scrutiny among traders and economists as its correlation to the actual official government labor report is less than 0.3. Last Thursday, however, featured what was perhaps the biggest market response to the report in many months.

ADP Payroll Details: Strong Small Business Hiring Activity, Job Cuts Among Large Corporations

The survey revealed that private employment rose by a net 497,000 jobs in June, the most since February 2022 and far exceeding the consensus estimate of less than 230,000. The services sector was on fire with a 373,000 gain, led by a hiring pickup in leisure and hospitality. Job losses were seen in the information and financial activities sub-groups.

What was particularly encouraging (and hot from the Fed’s perspective) was that small businesses added 299,000 positions, but wage gains softened, per ADP.

Treasury Yields Rise Amid Some Hot Data

Like so many macro data points, it’s often more about the market’s response to such news that really matters. In this case, the June jobs gain, more than twice expectations, sent the bond bulls running for cover.

Yields jumped across the Treasury curve with the 2-year note’s rate jumping above 5%, briefly surpassing its pre-SVB cycle high. The yield on the 1-year bill is now higher than 5.4% - easily above the March 2023 peak as more Fed rate hikes are priced in and there’s scant chance of cuts anytime soon.

Key for corporate executives and prospective home buyers alike, the 10-year Treasury rate settled last week at 4.05% - just a stone’s throw from notching the loftiest level since October last year when the stock market made its 2022 low.

Equities Hold Serve Ahead Q2 Earnings

Stocks, meanwhile, initially fell significantly, but not dramatically, after the Thursday morning report. A midday rally helped the S&P 500 avoid too steep of a daily slide. That is an encouraging sign for the bulls – the market has generally been taking the so-called “higher for longer” interest rate situation and expectation in stride.

Recall it was just a few months ago when short-term yields were significantly lower and Fed rate cuts were baked into the futures curve starting as early as this quarter. Now, however, following last week’s labor market data onslaught, no cuts are expected until the middle of next year, according to the CME FedWatch Tool.

Jobless Claim Steady

ADP was not the only macro news that moved markets. Initial jobless claims verified about in line with expectations. Recall those two weeks in June where this leading indicator pointed to a fall-off in the labor demand situation, but those were caused by one-off state issues (namely with Minnesota and Ohio). The 248,000 initial claims figure still suggests employment in the US remains robust. Friday’s official NFP jobs report backs up that assertion.

Hot ADP, Lukewarm NFP

Last Friday morning, the Labor Department reported that June featured a 209,000 net employment gain, slightly less than what economists had expected, but not a terrible number. It was, though, the first headline miss since April of 2022 and the softest print since a negative payrolls change in December of 2020.

Revisions to April and May were significant at –110,000 and countered ADP’s gangbusters report. The household survey used to generate the unemployment rate was a bit stronger at +273,000 jobs. The unemployment percentage itself ticked down to 3.6%, but that matched the consensus.

Wage gains remained robust, however, with wages rising at 0.4% from May and higher by 4.4% from a year ago. Average weekly hours came in a tenth of a percentage point hotter than expected, but that merely partially offset May’s steep decline.

A Ho-Hum Summer Friday After the Labor Market Report

Stocks were whippy around the Friday pre-market release. The S&P 500 managed to rise throughout the morning, but then selling pressure ensued in the afternoon, leading equities to finish lower for the holiday-shortened week. Other key data last week included fresh monthly reads from the Institute for Supply Management (ISM): The Manufacturing survey came in soft at 46.0 (an 8th consecutive sub-50 reading, indicating contraction in that slice of the economy) while the Services ISM was a tad hotter than forecast at 53.9 (of course, the US is much more a services-based economy versus manufacturing). The good news is that the ISM Prices Paid sub-indexes suggest modest inflationary pressures for now.

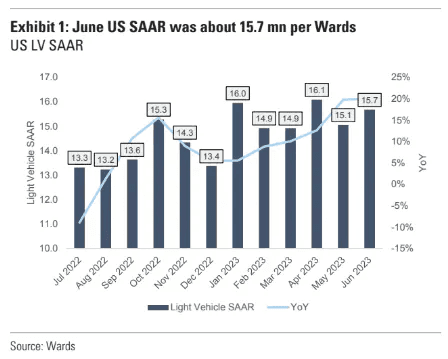

Data Spotlight: Auto Sales Suggest Consumers Keep Spending

Something that investors should also take note of was June’s robust 20.2% year-on-year rise in US vehicle sales. The 15.7 million seasonally adjusted annual rate, according to Wards, confirms that consumers are willing to take on higher auto loan rates, and doling out cash along with making higher interest payments puts a strain on overall excess savings from the pandemic era.

The consumer is closer to being tapped out from that measure. But with wages now rising at a faster pace than inflation, the ‘no landing’ narrative is that labor income will be enough to offset falling savings.

Improving Light Vehicle Sales Trends as Supply Chains Loosen

Source: Goldman Sachs

From the Macro to the Micro

Earnings season will become front and center among macro analysts and individual stock investors alike. The big banks will certainly offer fascinating clues as to the state of the lending market and capital market conditions. In particular, words from JP Morgan’s chief Jamie Dimon and CEOs from other large financial institutions will be interesting considering that the IPO market has shown signs of un-freezing (so to speak).

At the same time, the ongoing looming recession (some call it the ‘Godot’ recession) remains a risk with second-half US real GDP growth rate estimates near 0% despite second-quarter GDP looking to have been near 2% on an annualized basis.

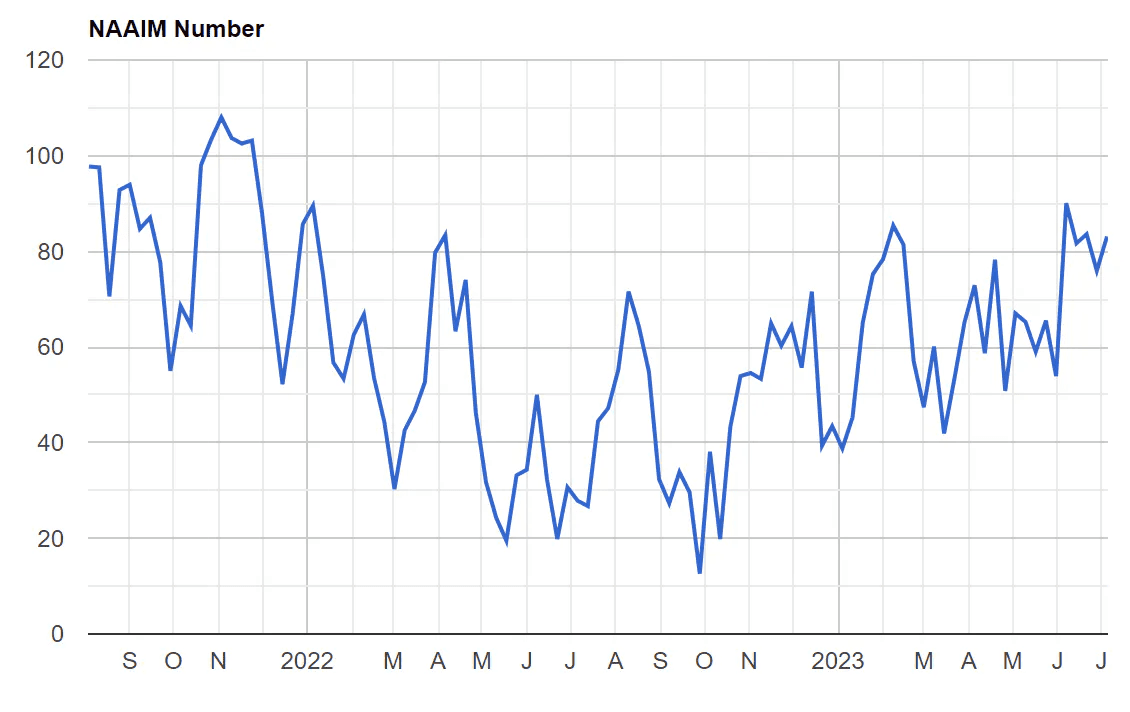

Investor Enthusiasm is Strong. Is that Reason Enough to Take Caution?

Price action suggests a possible cooling-off period for global equities. Our team spots bearish divergences between momentum and price developing, and that was confirmed last week by the sideways to marginally lower performance trend. Another thing to keep in mind is that investor positioning is by no means bearish any longer.

In fact, both the AAII Sentiment Survey (which the Macro Money Monitor has called out previously) shows a heavy net bull position and the National Association of Active Investment Managers Exposure Index took a leg higher to 83.1 from 75.9 in the prior week. Still, July remains a historically strong month (the NASDAQ has not had a loss in July since 2007), but the real action may not come until the month’s final full week – that's when the next Fed rate decision takes place and when mega-cap tech earnings hit the tape.

Last week’s Alpha Blog offers color on why late July could see a volatility jump.

NAAIM Exposure Index Rises in Early July

Source: NAAIM

Earnings Season Expectations Appear Tame

With still-decent labor market conditions, rising real wages, and higher interest rates, investors will surely keep their eyes glued to the upcoming round of earnings reports and their ears tuned to conference calls. As it stands, strategists expect a 7.2% decline in year-over-year S&P 500 earnings per share, which would be the largest EPS drop since Q2 2020. With 67 SPX companies issuing negative earnings guidance so far, compared to just 46 upward revisions, profit estimates have retreated from the end of Q1, according to FactSet.

EPS Estimates Near Their Lows

This reporting period is key as it likely marks trough earnings for firms. The Q3 estimated EPS growth rate is 1.2% while the fourth quarter is expected to feature a 3.4% annual earnings rise. All of this comes as calendar year 2023 and 2024 EPS estimates are steady or even fractionally lower over the last several weeks.

Next-12-months per-share profit totals are near $232 ($220 for ‘23 and $246 for ‘24), so the S&P 500’s P/E ratio remains high near 19. So, we would describe the earnings bar as not overly high, and without any major macro hiccups lately, US corporations should be able to top estimates, but investors must pay close attention to forward guidance as well as how stock prices react during this reporting season.

The Bottom Line

Stocks meandered lower last week as volume was generally light across the major exchanges. The VIX spiked to the mid-teens (it’s hard to deem that a true jump) while the US dollar retreated modestly. The domestic labor market remains healthy despite mixed reports for June.

The economy continues to see a weak manufacturing sector but healthier services trends, according to soft data readings from supply managers, while hard data points are more robust. In net, sufficient evidence exists for the Fed to keep its foot on the economic brake pedal. A quarter-point rate rise is expected come July 26 and corporate earnings season will shed new light on how the macro picture may look in the second half.

Want access to your own expert-managed investment portfolio? Download Allio in the app store today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.