Updated October 26, 2023

Bill Chen, CFA

Personal Finance

If you consume enough content about investing, you’ll eventually hear somebody say that the market is forward-looking. What this means is that the market doesn’t necessarily reflect the current state of the economy, but future expectations.

Of course, reality rarely ever meets expectations perfectly. These mismatches between expectation and reality are ultimately a major factor that contributes to volatility in asset prices, as the market is constantly adjusting and recalibrating as more data becomes available.

Usually, these recalibrations happen in response to events that are unexpected, but not necessarily unheard of: Missed earnings, a spike in unemployment figures, actions taken by the Fed. They may not have been expected, but they are a known threat—a possibility that can, and should, be factored into portfolio construction.

But every so often, something will happen that is so awful, and so outside of the realm of what is expected that it takes investors completely by surprise. Because such an event is almost never considered a possibility until after it has happened for the first time, most investors have not prepared for them. This often leads to dramatic market adjustments.

These surprise events are called black swans. The name comes from the fact that, until the first black swan was discovered, it was assumed that all swans were white.

The September 11 terrorist attacks in 2001, the collapse of Lehman Brothers in 2008, and the emergence of COVID-19 in 2020 are all examples of black swans events that had serious impacts on the market. But black swan events don’t just occur in the market. They can also occur in our everyday lives: Unexpected moments that threaten to derail our finances.

Below, we walk through a few examples of what black swan life events can look like and also discuss some steps that you can take to help yourself prepare for the unexpected.

Black Swan Life Events

In our personal lives, black swan events are rarely ever as rare or as paradigm-shattering as they tend to be in the world of investing. Instead, they tend to be surprise expenses that pop up when we least expect them. When they do pop up, they can be incredibly disruptive not just to our lives, but to our finances as well.

That’s especially true if you are like the 56% of Americans who have less than $1,000 in savings.

One example that is commonly discussed is a surprise car expense, such as a flat tire or blown transmission, which might cost a few hundred or a few thousand dollars to resolve depending on the severity of the problem.

Because most people depend on their vehicles as their primary mode of transportation, such a repair becomes critical. Without it, how would you get to work? How would you bring yourself (or your children) to the doctor, or to school? How would you go grocery shopping?

In such a case, someone who did not have the savings to cover the expense would be forced to find another way to pay for it. Friends or family might be able to help, but borrowing money can often be a strain on relationships. Credit cards might come in handy in a pinch, but these carry high interest rates that just make the expense even more expensive. The same goes for payday loans. Pawn shops might offer fast cash if you have something to sell, but you’ll rarely ever get the full value of whatever it is that you’re selling.

In other words, by failing to anticipate and prepare for the expense, we force ourselves into even riskier and more precarious positions.

Some other examples of expenses that often take people by surprise might include:

A broken tooth requiring immediate treatment by a dentist

An injury or illness making it impossible to work for a period of time

A surprise home repair such as a broken window, roof, or appliance

An emergency cross-country trip to attend the funeral of a loved one

Unexpectedly losing your job and being unable to find new work

How to Protect Yourself

In some cases, having the right types and amounts of insurance coverage can help you weather life’s most drastic black swan events. Dental and health insurance may be able to help you cover those unexpected medical events; homeowners insurance may help you with a repair; life insurance can help protect your family in the event you were to die unexpectedly.

But in many cases, insurance doesn’t exist to help you cover these unexpected expenses. (And even if it does, you’ll likely need to meet a deductible by paying for a portion of the expense out of pocket before insurance does kick in.)

With this in mind, it is critical to have an adequate emergency savings fund to help you pay for those things that insurance can’t.

Building Your Emergency Fund

If you do not have an emergency fund, use the following steps to get started:

1. Determine how large your emergency fund needs to be.

Most financial experts recommend that the average person should have between 3 and 6 months’ worth of expenses set aside in their emergency fund. This will usually be enough of a cushion to cover the most common emergency expenses that life will throw at you, and can also see you through a short period of unemployment while you look for a new job.

That being said, the right amount for you will depend on a number of factors, including your personal financial situation, risk tolerance, and ability to find a new job after a job loss. The 3-6-9 guideline can help you determine what the right amount is for you:

3 months’ worth of expenses: This may be enough of a cushion for you if you believe that it would be relatively easy to find a new job in the event that you were to lose your current one, and if you have relatively few obligations (in the way of a mortgage, children to support, etc.).

6 months’ worth of expenses: If you believe that it will still be easy to find a job if you lose your current one, but have serious obligations impacting your finances, 6 months’ worth of expenses is likely a better target. This is especially true if you have children to support or a mortgage to pay, as it is very difficult to reduce the expenses tied to these obligations.

9 months’ worth of expenses: Generally speaking, you will only need 9 months’ worth of expenses if you have an unsteady source of income. For example, if you are a full-time freelancer, work a seasonal job, or are self-employed, a larger cushion can help see you through slow times. This may also be an adequate amount if you work in an industry or at a business which is struggling and expect that it may be difficult to find a new job if you lose your current job.

It should be noted that the 3-6-9 guideline is just that: A guideline. Only you can decide how big of an emergency fund is right for you

2. Make a budget.

If you don't already have a budget, you need to create one. This will allow you to track your spending and identify areas where you can potentially cut back on your expenses in order to free up money for other goals, such as building an emergency fund.

Once you have a budget, it’s crucial that you include your emergency fund as a line item in it. This will ensure that you are consistently paying yourself first and working toward your savings goal each and every month. It will also help you break down your goal into smaller, more manageable pieces, which increases the chances that you will stick with it over the long run.

How much should you be saving each month? This will depend on how much money you have available in your budget (or how much money you can free up in your budget) to dedicate toward savings.

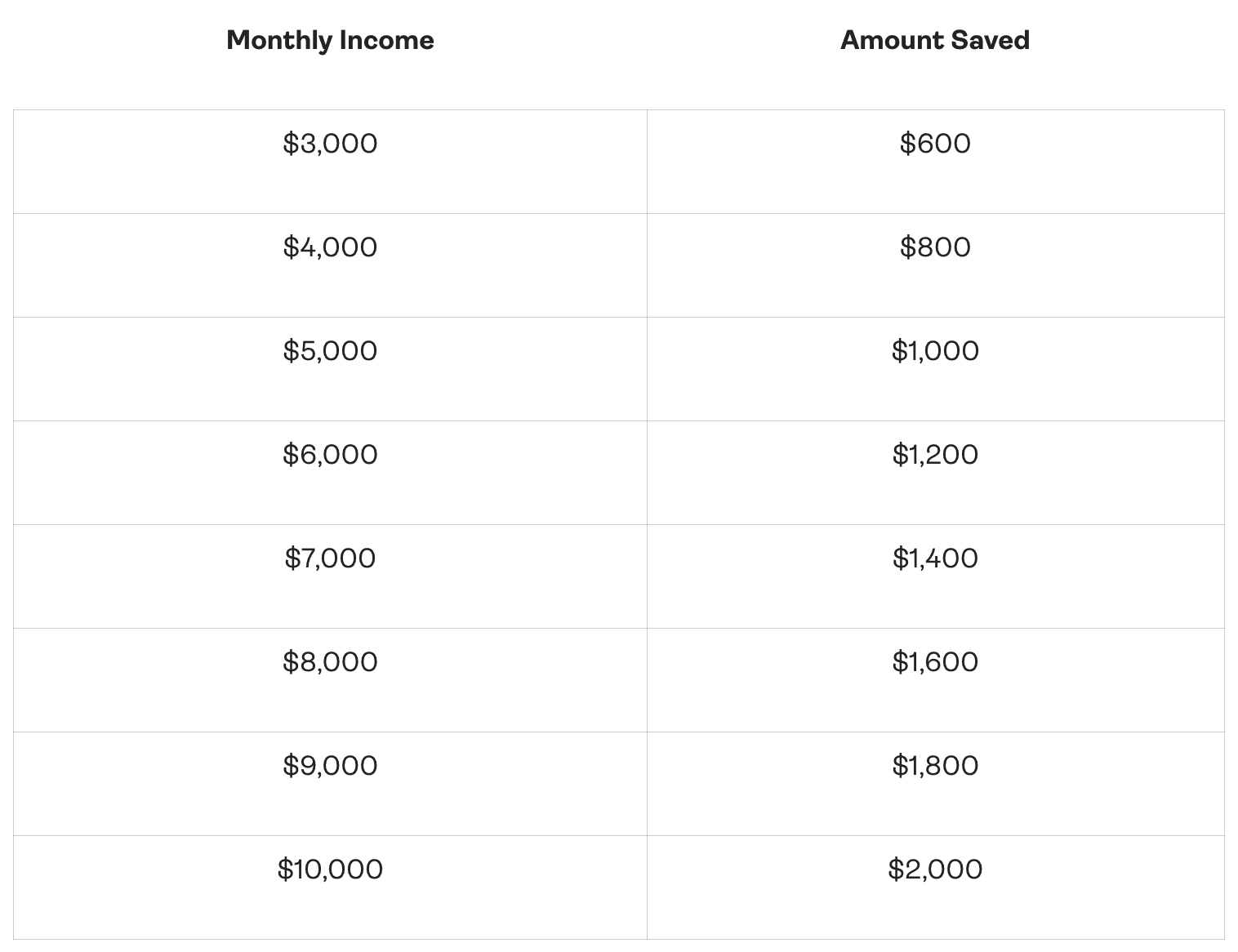

The specific budgeting strategy that you leverage may also dictate that you use a certain percentage of your income each month to reach your savings goals. For example, the popular 50/30/20 rule states that 50% of your net income should be dedicated to your “needs” and 30% to your “wants.” The final 20%, then, is dedicated toward your savings goals.

The following table shows what this would look like for a range of monthly incomes:

Once you know how much money you have in your budget to dedicate to building an emergency fund, you can set yourself a time-bound goal for completing it.

For example, imagine that your net income is $4,000 per month. You determine that a 6-month emergency fund for you would contain $15,000. Using the 50/30/20 rule outlined above, you would be dedicating $800 each month toward your emergency fund. By dividing $15,000 by $800, we see that it would take just under 19 months to reach your goal.

3. Leverage automation to streamline your savings efforts.

This last step is optional, but highly recommended.

Now that you know how much money you are going to save every month, consider automating your savings. You can do this by setting up a recurring transfer from your checking account into your savings account, either on a monthly, bi-weekly, or weekly basis (depending on how often you get paid).

Automating your savings can be a very effective means of keeping you on track as you work toward your goal. That’s because automation reduces friction. When you automatically transfer a certain amount of money from your checking account into your savings account, you no longer need to think about it or make a conscious decision to save. It’s simply something that happens in the background. The fewer times you need to actively make the decision to save, the fewer chances you give yourself to change your mind—and the better off you’ll be in the long run.

Here at Allio, we’ve got a number of tools that you can use to work towards your financial goals, whether that is building an emergency fund or investing for the future. For example, our recurring transfers function allows you to automatically save or invest on a recurring schedule—perfect for those looking to automate their efforts.

Likewise, if you ever find yourself with a surprise windfall (perhaps from a work bonus) you can make a lump-sum deposit. More of a spender? Turn on our round-ups function to save money automatically every time you make a purchase with a linked debit or credit card.

Whether you’re seeking an expert team to manage your money or looking to build your own portfolios with the best financial technology available, Allio can help. Head to the app store and download Allio today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.