Updated October 17, 2023

Bill Chen, CFA

Personal Finance

If you’re a tax-conscious investor, then chances are pretty good that you’ve heard the term tax-loss harvesting thrown around here or there. And for good reason—tax-loss harvesting can be a really effective means of leveraging investment losses in order to reduce your tax burden.

But tax-loss harvesting isn’t the only strategy that you can use to reduce your tax bill. In fact, sometimes it can be beneficial to engage in tax-gain harvesting. This can be especially true for younger investors, or those who are currently in a lower tax bracket but expect that they will eventually move into a higher bracket.

Below, we define capital gains and capital losses, tax-loss harvesting, and tax-gain harvesting. We also take a closer look at the different scenarios in which it might make sense for an investor to engage in tax-gain harvesting.

Capital Gains and Capital Losses

When you purchase an asset as an investment, its price will naturally fluctuate over time—sometimes up, and sometimes down.

If the price goes up, the difference between what you paid for it and its current price is known as an unrealized capital gain. If the price goes down, the difference between the price you paid for it and its current price is known as an unrealized capital loss.

Those gains and those losses remain unrealized for as long as you continue holding the asset. But once you sell the asset, they become locked in as either a profit or a loss. Both of these scenarios will trigger tax implications.

When you realize a capital gain, you’ll have to pay what’s known as a capital gains tax. How much you owe will depend on how long you held your investment.

Short-term capital gains arise when you sell an asset for a profit less than one year after you bought it. Short-term capital gains are taxed at your ordinary income tax rate.

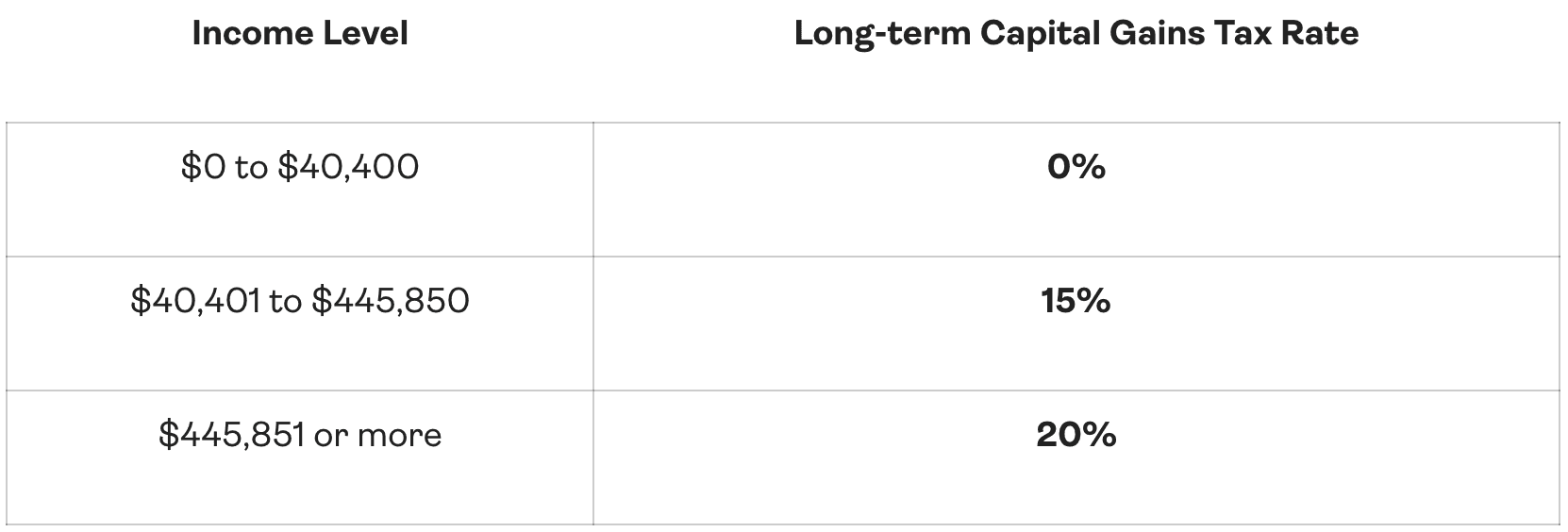

Long-term capital gains, on the other hand, arise when you sell an asset for a profit after holding it for at least one year. Long-term capital gains are taxed at a more favorable tax rate, which is dependent on your annual income. The chart below shows the long-term capital gains tax rates in 2022 for single filers:

When you realize a capital loss, however, you won’t pay any taxes. In fact, those losses can help you to reduce your tax bill.

Capital losses are first netted against your capital gains, depending on whether they are short-term capital losses or long-term capital losses. This means that long-term capital losses netted against any long-term capital gains you may have realized in the year, while short-term capital losses are netted against short-term capital gains. If there are any capital losses left over, they will be netted against any capital gains that remain. If there are still any capital losses after that, they can be used to offset up to $3,000 of income in the current year—and if there are still losses, they can be carried forward to reduce your tax bill in future years.

What is tax-loss harvesting?

Tax-loss harvesting is a tax management strategy that involves selling a selection of losing investments each year to offset realized capital gains.

Typically, the strategy also involves replacing those losing positions with similar investments so that the overall composition of your portfolio remains virtually the same. This allows you to enjoy a reduction in taxes without needing to sacrifice your overall investment strategy or target asset allocation.

For example, let's say we purchase $1,000 of XLF, an ETF that tracks the financial sector. Let's suppose that in one year's time XLF has lost 10% of its value, so that our position is now worth $900. Let's further suppose we did additional rebalancing of our portfolio during the year and ended up with $100 in realized short-term capital gains that we now owe taxes on.

If we were to sell XLF and take the $100 short-term loss, we could use that loss to offset our $100 gain. At the same time, we could replace XLF with IYF, another ETF in the financial sector, so that our portfolio composition remained essentially unchanged. But now, we would owe nothing in taxes (because our $100 loss on XLF would offset our $100 gain on the rest of the portfolio).

As taxes are one of the most powerful forces that threaten your journey toward building wealth, tax-loss harvesting can have a major impact on the performance of your portfolio over time. But it’s also not the only way that you can manage your taxes. In some cases, tax-gain harvesting might be more beneficial.

What is tax-gain harvesting?

Tax-gain harvesting is a tax management strategy that involves selling assets in order to realize a capital gain. This will trigger capital gains taxes in the year in which the asset is sold.

Tax-gain harvesting makes the most sense when you find yourself in a lower tax bracket than you expect you will be in in the future. This is why tax-gain harvesting can be a powerful tool for younger investors who are in the earlier stages of their career.

As an example of how tax-gain harvesting works, let’s take a look at the following scenario.

Patricia is a 25-year old who currently works as a part-time barista at a coffee shop while she finishes her college degree. Her annual salary is $25,000. When she graduates and finds a job in her field, she expects to be making closer to $60,000 per year.

When Patricia was 20 years old, she used her birthday money to buy $1,000 worth of an ETF. In the years since, the shares have doubled in value, and she has been considering cashing out her investment so that she can use the money to buy a new car. But she isn’t sure if she should do so now, or when she graduates the following year.

At her current salary, Patricia’s long-term capital gains tax rate is 0%. This means that if she was to sell her shares now, she would owe no taxes on the profit. But if she was to wait until next year, when her salary was higher, she’d find herself paying 15% of that profit ($150) as capital gains taxes.

Since Patricia already plans on selling the investment and using the money for a specific purpose, she’d be better off from a tax perspective to tax-gain harvest now before her income rises.

As mentioned above, tax-gain harvesting can make a lot of sense for younger investors and those who are early in their careers, who expect their income—and tax rates—to rise in the future. It can also be helpful for individuals who find themselves temporarily in a lower tax bracket, such as someone who takes a sabbatical, a “mini retirement,” or who moves to part-time work.

The Right Strategies at the Right Times

At the end of the day, both tax-loss harvesting and tax-gain harvesting can be powerful tools that help you minimize and manage your tax burden. While a few percentage points here and there may not seem all that substantial, over time it really does add up.

Allio is here to help you work toward your financial goals. Our goal is to provide clients with the tools and strategies they need—when they need them—at each point in their investment life-cycle.

Whether you’re seeking an expert team to manage your money or looking to build your own portfolios with the best financial technology available, Allio can help. Head to the app store and download Allio today!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.