Updated September 18, 2023

Adam Damko, CFA

The Piggy Bank

THE MARKETS

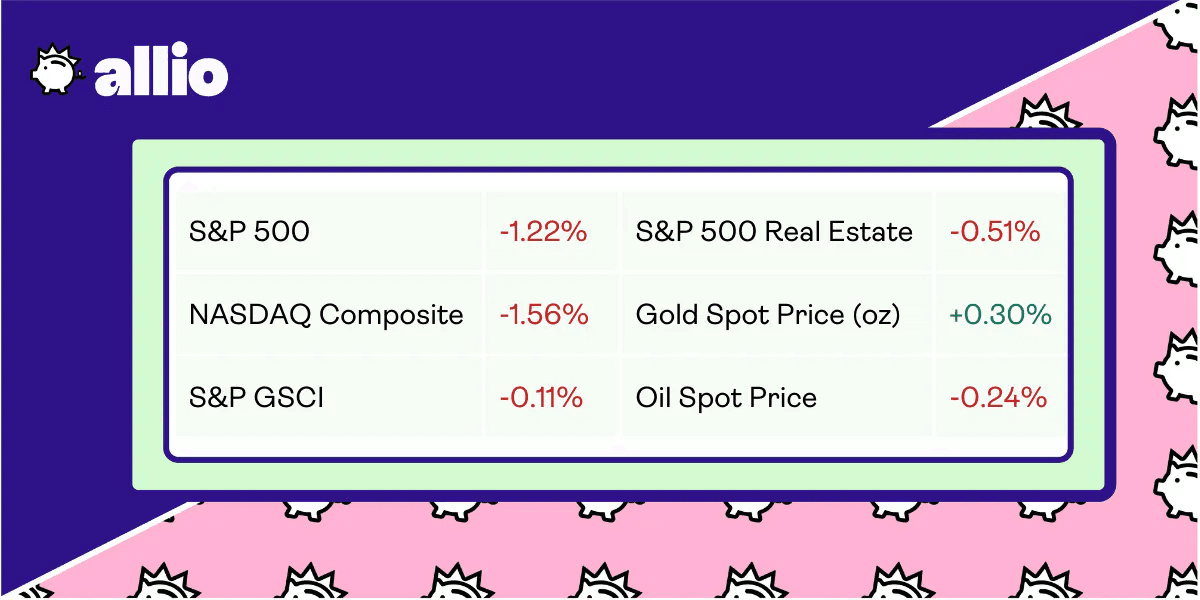

📈 Markets tumbled this week, giving back ⅓ to ½ of their prior week’s gains, as macro concerns about Europe and China took center stage.

💼Economic News

Thanks to rising inflation and falling wages, US poverty rose in 2022. This rise in US poverty was fueled by the expiration of pandemic-era stimulus benefits, mainly the child tax credit.

Continuing the streak of financial challenges for Americans, it was announced that the inflation-adjusted median household income fell to $74,580 in 2022, down 4.7% since its peak in 2019.

Ending on a positive note, California fast food workers have secured $20 per hour standardized paychecks. This is a hike from the current minimum of $15.50, which was already the highest in America. The announcement is the result of a deal between labor unions and restaurants. As major strikes rage on in the entertainment and now auto industries, it’s a promising sign to see workers and employers reaching agreements without labor disputes.

👀 What to Be on the Lookout for This Week

The biggest event to keep an eye on is the Federal Reserve’s latest decision on whether or not to raise interest rates at its September FOMC meeting. More on that below.

Additionally, there are a number of economic releases and earnings reports to keep an eye on.

Economic releases:

Monday: NAHB/Wells Fargo Housing Index

Tuesday: Building Permits, New Housing Starts

Wednesday: Fed Interest Rate Decision

Thursday: Jobless Claims, Existing Home Sales

Earnings releases:

Monday: Stitch Fix

Tuesday: Autozone

Wednesday: FedEx, General Mills

Thursday: Darden Restaurants

📰 In Other News

As is often the case in the US, Big Tech dominated the headlines this past week.

First, US lawmakers are officially pushing forward with plans to regulate generative artificial intelligence. The new technology is still in its Wild West phase. To reel it in, US legislators are pushing new regulatory guidelines and meeting with the resident gunslingers of the AI industry, including Elon Musk, Meta’s Mark Zuckerberg, OpenAI’s Sam Altman, Microsoft’s Brad Smith, and more.

So far, the proposed plan is to introduce a licensing system for companies that work on “high-risk” AI models. Under this system, companies developing more complex models would be required to obtain a license, while startups working on simpler AI projects are off the hook.

In other Big Tech news, Google is currently locked in the biggest antitrust trial in twenty years. US regulators accuse the company of owning a monopoly in internet search. This is mainly due to the strategic partnerships Google has in place with other tech players. For example, Google pays billions of dollars annually to be the default search engine on Apple products.

The trial could result in Google being broken up into smaller companies. But experts say that result is unlikely. Instead, Google could face multiple restraints on its current business practices.

Finally, TikTok has officially launched its ecommerce shop in the US. Given the company's size and cultural influence, this move could pose a significant threat to other companies operating in the online shopping space.

Reflects performance at market close 9/15/23

INFLATION UPDATE

🔺Inflation Spikes 3.7% In August

August Inflation

In August, the annual inflation rate hit 3.7% — the second straight month of acceleration — up from 3.2% in July.

The rising cost of energy was one of the main drivers of inflation. In August, energy prices rose by 5.6%, mainly due to a 10.6% increase in gasoline prices. Food prices also rose 0.2%, and shelter costs climbed 0.3%.

The good news is that inflation slowed for electricity (2.1% vs 3% last year), food (4.3% vs 4.9%), shelter (7.3% vs 7.7%), new vehicles (2.9% vs 3.5%), and apparel (3.1% vs 3.2%). Inflation was also down for airfares (down 13.3%) and used vehicle prices (down 6.6%).

Federal Reserve officials prioritize core CPI, as it provides a better indication of where inflation is heading over the long term. In August, core CPI — which excludes volatile food and energy prices — rose 4.3% annually, down from 4.7% in July.

This was the fifth consecutive month that core inflation has slowed.

In Perspective

Over the past year, people all across the country have hoped for the end of this era of record-high inflation. Moderating inflation over the past few months encouraged this sentiment. But the latest data shows that, although inflation has declined considerably compared to last year, the US may not be entirely out of the woods just yet.

Up until July, Americans enjoyed nearly a year of decreasing inflation. Experts hoped that July's 3.2% annual increase was just a temporary blip. However, with inflation rising yet again in August, central bankers may feel the need to take more decisive action.

The Federal Reserve has consistently reiterated a target annual rate of 2%. Both annual CPI and core CPI are well above this target — and trending in the wrong direction.

Where Do We Go From Here?

Ultimately, it's unlikely that this most recent report will lead to a significant shift in the Federal Reserve's current position.

The central bank has been gradually increasing its benchmark borrowing rate since March 2022, which currently sits at 5.25%-5.5%.

Since this spike in inflation was not too drastic, it's likely the Fed will maintain current interest rates during its next meeting. Still, the possibility of an additional rate hike before year’s end remains. In fact, the market is currently factoring in a 40% chance of a final rate increase in November.

For consumers, if the Fed continues to raise rates, the cost of borrowing money will continue to increase. This jump in inflation has also hit worker paychecks, with real average earnings declining 0.5% for the month. On the plus side, they remain up 0.5% year-over-year.

Still, not all is lost. The story told by economic data could always change by November, and the Federal Reserve's stance is sure to shift with it.

YOUR ECONOMY

💰 Should You Swap Your Kid’s Allowance for an IRA?

Planting Seeds

For teenagers and pre-teens, the idea of saving for retirement might sound absurd. After all, why should young individuals start thinking about retirement when they haven't even finished high school? But there's a compelling reason why: compound interest.

Despite their probable lack of financial literacy, a 10-year-old investor has quite an advantage over a 30-year-old investor. Those extra twenty years add up. They’ll soon be watching their savings grow and compound year after year.

Teaching children about long-term investing (not trading) and general financial literacy helps to set them up for a secure future.

Benefits of a Roth

A Roth IRA is a highly popular investment vehicle because it allows money to grow tax-free. These accounts typically track a wide range of diversified equity and fixed-income investments. As of 2023, investors are allowed to contribute up to $6,500 per year.

A child’s guardian can contribute to their Roth IRA, but the contribution cannot exceed the child’s earnings. For instance, if a child earned $1,000 from babysitting during the summer, a parent, guardian, or grandparent can contribute up to $1,000 to the child’s IRA.

Another benefit often overlooked in Roth IRAs is that, for certain purchases, owners can access contributions without paying a penalty. For instance, up to $10,000 can be withdrawn tax and penalty-free for the purchase of a home. This flexibility is an ideal choice for parents looking to provide their children with a strong financial foundation.

Getting Started

The ideal time to open an IRA for a child is when they're young. The second best time is now.

Children eighteen or older can open a Roth IRA on their own. Children under eighteen will need an adult to act as a custodian. Parents will still be able to transfer the account into their child’s name at eighteen.

Parents can open an account at any age. Although sooner is always better, most accounts see the bulk of their funding when children are old enough to take on a part-time or summer job. It’d take a pretty successful lemonade stand to make a major contribution — but, after 20 years of compound interest, even $50 a year would be meaningful.

🤷 The Secret To Achieving More? Trying Less

Giving It 85%

Americans are taught from day one to give their absolute best, aiming for that perfect 4.0 GPA, and striving for a flawless SAT score. This drive for excellence extends throughout our lives. From personal endeavors to careers, the traditional American mentality is to give everything we do 110%.

But now that message is changing. Workers and business leaders alike are starting to embrace a different perspective. Research shows that pushing yourself to the extreme might not yield the best results.

Exercise physiologists say lifting heavy weights until exhaustion actually leads to less muscle gain, and the same appears to apply to business. Advocating for a balanced approach to peak performance, productivity coaches suggest a new golden rule: instead of giving it 110%, aim for about 85%.

By granting yourself a reasonable margin for error, you can decrease stress and boost your prospects for long-term success.

Doing Less, Achieving More

85% effort is hardly slacking off. You would still have to put in a lot of effort to reach the new magic number — just not so much effort that you leave exhausted and unable to do the same the next day.

Experts agree the trick is to skip the unnecessary stress over minor inconsequential details in the pursuit of perfection. Trimming off that top 15% from the goal helps us achieve this. Additionally adjusting standards to 85% helps transform the approach toward success from all-or-nothing into a more flexible spectrum.

This principle can also apply toward various aspects of one's personal life, including work, health, and hobbies. For instance, setting down a hard-fisted fitness goal of a one mile daily run could end in a week, if one day is missed. If plans have to change on a busy weekday, the 85% mindset allows for some leeway. Flexibility and consistency is key, allowing you to accommodate the occasional setback.

Learning From Mistakes

Allowing room for a small margin of error has another advantage: there's a lot to learn from mistakes. When we strive for perfection, we miss out on valuable lessons that come from minor setbacks.

This old idea holds true even in the new world of artificial intelligence. In a 2019 study, researchers found that a smart computer program learned best when it aimed to answer questions correctly 85% of the time. The 15% margin of error helped the program identify its mistakes and improve faster.

Ultimately, success is a spectrum. Achievements come in shades, not just black and white. By aiming for 85%, there’s plenty of room for mistakes — and none for stress.

POCKET CHANGE

Big pharma’s blockbuster obesity drugs could turn into a $100 billion market. Novo Nordisk and Eli Lilly are leading the industry with their drugs Ozempic, Wegovy, and Mounjaro.

Meta Platforms is working on a new AI model to rival GPT-4. The social media conglomerate plans to start training the new model in 2024.

Generative AI faces a generation gap. 75% of Generation Z has reportedly used generative AI, while 68% of non-users are Gen X or Baby Boomers.

Roughly 50% of consumers expect personal consumption to shrink in early 2024. This could potentially be the first quarterly decline since the onset of the pandemic.

50% of consumers plan to start holiday shopping before Halloween. At the same time, 40% of shoppers expect to feel financially burdened during the holiday season.

Invest your change, change your life. Head to the app store and download Allio today to start building wealth on autopilot!

Related Articles

The articles and customer support materials available on this property by Allio are educational only and not investment or tax advice.

If not otherwise specified above, this page contains original content by Allio Advisors LLC. This content is for general informational purposes only.

The information provided should be used at your own risk.

The original content provided here by Allio should not be construed as personal financial planning, tax, or financial advice. Whether an article, FAQ, customer support collateral, or interactive calculator, all original content by Allio is only for general informational purposes.

While we do our utmost to present fair, accurate reporting and analysis, Allio offers no warranties about the accuracy or completeness of the information contained in the published articles. Please pay attention to the original publication date and last updated date of each article. Allio offers no guarantee that it will update its articles after the date they were posted with subsequent developments of any kind, including, but not limited to, any subsequent changes in the relevant laws and regulations.

Any links provided to other websites are offered as a matter of convenience and are not intended to imply that Allio or its writers endorse, sponsor, promote, and/or are affiliated with the owners of or participants in those sites, or endorses any information contained on those sites, unless expressly stated otherwise.

Allio may publish content that has been created by affiliated or unaffiliated contributors, who may include employees, other financial advisors, third-party authors who are paid a fee by Allio, or other parties. Unless otherwise noted, the content of such posts does not necessarily represent the actual views or opinions of Allio or any of its officers, directors, or employees. The opinions expressed by guest writers and/or article sources/interviewees are strictly their own and do not necessarily represent those of Allio.

For content involving investments or securities, you should know that investing in securities involves risks, and there is always the potential of losing money when you invest in securities. Before investing, consider your investment objectives and Allio's charges and expenses. Past performance does not guarantee future results, and the likelihood of investment outcomes are hypothetical in nature. This page is not an offer, solicitation of an offer, or advice to buy or sell securities in jurisdictions where Allio Advisors is not registered.

For content related to taxes, you should know that you should not rely on the information as tax advice. Articles or FAQs do not constitute a tax opinion and are not intended or written to be used, nor can they be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer.